These Related Stories

Share this

Do you know what your net worth is? It's not too hard to calculate, and it's a good number to know as you work toward your financial goals.

Your net worth is your assets minus your liabilities -- or, as Investopedia puts it, "it’s the value of everything you own, minus all your debts." Net worth is one measure of financial success. It helps give you a real understanding of your overall financial position.

Your net worth can be a negative number, and this often happens for young professionals who are out of college but still working at paying off their student loan debt.

Calculating Your Net Worth

If you want to calculate your own net worth, here's how to do it.

- Make a list of your assets. This includes cash, checking and savings accounts, retirement accounts, investments, and assets like homes or cars.

- Add up the total amount of your assets.

- Then make a list of your liabilities -- or your debts, or what you owe. This includes credit card debt, student loan debt, mortgage loans, car payments, and so on.

- Add up the total amount of your liabilities.

- Subtract your liabilities from your assets. The number you get is your net worth.

How does your net worth stack up to your peers? And what can you do to increase that number as you work toward your financial goals?

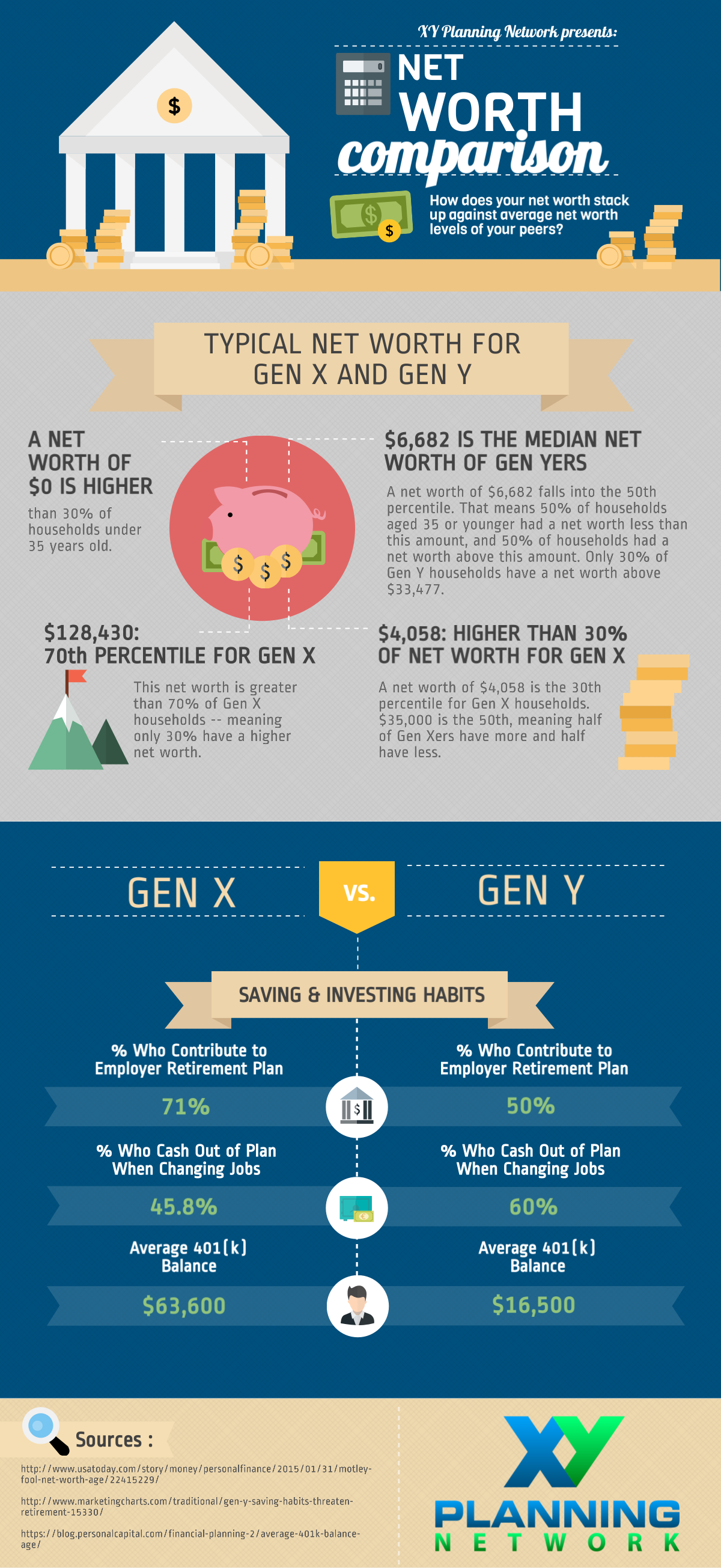

What's the Net Worth of Gen X and Gen Y?

We put together this infographic to help show the net worth of both Gen X and Gen Y. Check it out below -- we've also included a few notes on the saving and investing habits of these two age groups, which might explain the results.

You're welcome to share our infographic if you'd like. If you're publishing this somewhere, we ask that you provide a way for friends to find the original so please use this link: http://goo.gl/bIHxvR

How to Improve Your Net Worth

If you're not happy about the number you ended up with after you calculated your net worth, know that it is in your power to take action and change it. Here are some actionable tips to help you get started:

- Consider how you're saving for retirement (if you are at all). Are you contributing to an employer-sponsored plan if one is offered? Are you putting in enough to at least get the match? If you don't have an employer-sponsored plan, have you set up a traditional or Roth IRA? If you're self-employed, have you checked out your own retirement plan options? Remember, the sooner you start the easier it will be to build your net worth thanks to compound interest.

- Think about how you can earn more, and bank those raises. Saving is important, and it's easier to do when you earn more money. Negotiate your salary when starting new jobs, ask for what you're worth in your current position, and consider picking up a side hustle to boost income. When you do earn a raise, make a plan to invest at least half of it -- and make it an automatic contribution. You can add the other half to your budget to spend.

- Have a debt repayment plan. Know what you owe and have a plan to start aggressively paying off your debt.

- Work with a professional to map out a financial plan. It's not always easy to know exactly what you need to do next, and it may benefit you have a professional in your corner who can help you reach your biggest goals. Make sure any financial planner you work with is a fiduciary and has your best interests at heart. Need help finding someone qualified and who specializes in serving Gen X and Gen Y? Head over to our Find An Advisor portal.

How does your net worth measure up? What action steps can you take to increase your number?

Share this

Subscribe by email

A Millennial's Guide to Credit Reports

A Millennial's Guide to Credit Reports

July 28, 2018

4

min read

How to Become Rich: The Actions (and 3 Unexpected Habits) to Get There

%20to%20Get%20There.png)

How to Become Rich: The Actions (and 3 Unexpected Habits) to Get There

December 03, 2019

10

min read

Why Millennials View Finances Differently than Generations Before

Why Millennials View Finances Differently than Generations Before

December 29, 2018

4

min read