These Related Stories

Share this

“Financial institutions reported a total of $1.7 billion in suspicious activities in 2017, including actual losses and attempts to steal the older adults’ funds”, according to the Consumer Financial Protection Bureau.

Elder financial exploitation is incredibly common. It feels like people are constantly attempting to scam seniors.

Sometimes it is from an outside party, but other times, it is by someone the senior knows, such as a family member or friend.

Preventing senior financial exploitation is difficult; however, there are steps family members and friends can take to help protect our aging population.

Having worked with elderly adults for over a decade and based on my personal experience, I’ve learned there is no way to prevent elder financial exploitation entirely, but there are steps you can take to help reduce the likelihood of it happening.

Let’s look at eight tips to help prevent elder financial exploitation.

Tip 1: Set Up a Trusted Contact at Every Financial Institution

Thankfully, banks and investment custodians are designing new procedures to help combat senior financial exploitation.

Many banks and other financial institutions will ask you for a trusted contact. I know it can be easy to ignore it, but don’t!

It is important to take the time to set this up because a trusted contact is someone the financial institution can contact if there is a concern about you or something happening in your account.

Most people will list a family member or close friend, but it’s up to you.

A trusted contact can’t make transactions in your account or change any settings, but they can receive information from the financial institution to help administer an account.

Although a trusted contact isn’t a foolproof way to prevent elder financial abuse, it’s helpful to have another person the financial institution can contact if they suspect something is wrong.

Tip 2: Set Up “View-Only” Access for A Trusted Person

While a trusted contact usually is helpful once something has gone wrong, you are leaving the monitoring to the financial institution. Some people want to be more hands on, which is where setting up “view-only” access can be helpful.

While many people are tempted to put another family member on an account, many fail to understand the consequences of that action. If you add a family member as a joint account holder, you may be subject to gift taxes, open yourself up to more lawsuits, and eliminate certain tax benefits at death.

Instead, most people are better served by setting up “view-only” access or creating a financial power of attorney. I’ll talk about a financial power of attorney later.

“View-only” access is helpful because many banks and financial institutions allow someone other than the account holder to see transactions in the account.

For example, if you are an adult child who is worried about mom or dad’s spending, they may be able to set you up with online “view-only” access. Then, you can login as you please to view transactions.

I prefer online “view-only” access, but you can also often request duplicate statements be mailed to you. I don’t like this method as much because more than a month could pass before you find something suspicious. Also, if something happens, you won’t be able to login immediately and see the transaction.

It can be time-consuming and exhausting reviewing a loved one’s transactions, but if you set aside 10 minutes each week, you probably will quickly spot anything out of the ordinary.

As people age, I often recommend consolidating accounts. This is another good reason to consolidate accounts. If you only have one or two bank accounts and one custodian for investments, it’s much easier to monitor.

Another option is to subscribe to a monitoring service.

While I have never used it, EverSafe looks like a compelling service to help monitor and alert you to signs of scams, unusual spending patterns, and late bills.

Instead of manually reviewing transactions, EverSafe appears to look at historical behavior to see what is normal and flag unusual withdrawals, changes in spending, late bills, and more. Then, a “trusted advocate”, such as a family member can receive alerts.

I can see this being helpful for those who are busy and don’t want to review every transaction, but instead, want to be notified any time the system identifies a concerning financial transaction.

EverSafe has different tiers, and they cost anywhere from $77 to $255 a year, which is a small cost considering elder financial exploitation is often in the tens of thousands of dollars.

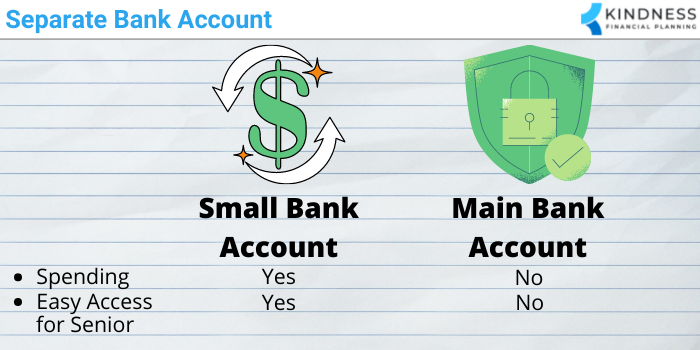

Tip 3: Create a Small Separate Bank Account

Creating a small separate bank account is an extreme solution, but is often necessary for people with cognitive impairment or other health issues that make them more prone to financial exploitation.

The strategy here is to have a main bank account with the bulk of their money and a smaller bank account they have everyday access to use.

You could put $500 or any amount that feels reasonable in a checking account with a debit card and check writing capabilities. It will be used for everyday spending, and the rest of their money will go in a separate bank account. As money gets spent in the smaller checking account, you can transfer money from the main bank account to the smaller account.

Although it can feel a little like an allowance as a child, it’s a way to protect the bulk of their savings they worked a lifetime to create.

If someone gains unauthorized access to the smaller account, they try to make a large purchase, or try to transfer a large sum of money, the most they can lose is what you put into the account.

Unfortunately, it’s very easy for people to take advantage of seniors, particularly those with declining cognitive function.

Below is a list of common scams, which could easily talk someone out of tens of thousands of dollars.

- Pretending to be from the government (unpaid taxes, unpaid property taxes, Social Security will be cut off, etc.)

- Computer tech support (message pops up claiming to be support, and your loved one gives access to their financial accounts)

- Charity scams (claim to raise money for a cause, but pocket the money instead)

- Robocalls (call claiming they won a sweepstakes or lottery and need payment to gain access to the prize)

- Online dating financial exploitation (start “dating” someone online who asks for money to come visit)

- Family emergency scams (call claiming a relative is in danger and they need funds immediately)

In a world where financial exploitation is a big industry, it’s tough to prevent scams entirely, which is why a separate bank account with a smaller amount of money is a good line of defense to prevent larger sums from being transferred.

Tip 4: Create a Durable Financial Power of Attorney

While view-only access to financial accounts is helpful, it doesn’t allow you to do anything with the account when things go wrong.

This is where a financial power of attorney or durable financial power of attorney can be helpful.

While a financial power of attorney is no longer effective once someone becomes incapacitated, a durable financial power of attorney continues even after becoming incapacitated, which is why I favor a durable financial power of attorney over a regular financial power of attorney.

Either way, a financial power of attorney can help you manage someone’s finances. To what extent depends on how the document is written.

Often, it will allow you to pay someone’s bills, transfer money among accounts, make investment transactions, file and pay taxes, and open and close accounts.

A financial power of attorney is instrumental because if an elderly person falls victim to a scam, they may be unable to report it or know how to prevent future unauthorized access.

With a financial power of attorney, you could step in to communicate with the financial institution about next steps and help your loved one recover from it.

Plus, if a loved one falls, breaks their hip, and they need to be hospitalized and go to a skilled nursing facility to recover, they may be unable to manage their finances. They may also have cognitive issues with sundowning or while on pain medication. This makes them more susceptible to being exploited.

With a power of attorney, you can help pay their bills and keep their financial life running smoothly. Since you are actively involved, there may be less of a chance they fall victim to a scam while they are unable to stay up to date on their finances.

Tip 5: Freeze Their Credit

I recommend everybody freeze their credit, but it’s even more important for elderly people.

If people are not checking their credit reports regularly, they often only find out about issues when they go to apply for new credit. Since elderly people are rarely applying for new credit, they may not find issues for years.

A credit freeze should help prevent scammers from applying for credit in someone’s name. For example, if a senior’s personal information was stolen and a scammer applied for a credit card in their name, the credit card company is going to want to look at their credit history from one of the three credit reporting agencies.

If the credit report is frozen, they likely won’t issue the credit card because they are locked from seeing the credit report.

Ever since Equifax, one of three major credit reporting agencies, had a data breach in 2017, I believe everybody should freeze their credit.

It’s easy to freeze online, and if you need to unfreeze it to apply for credit, you can temporarily unfreeze it for a day or two while your credit report is ordered.

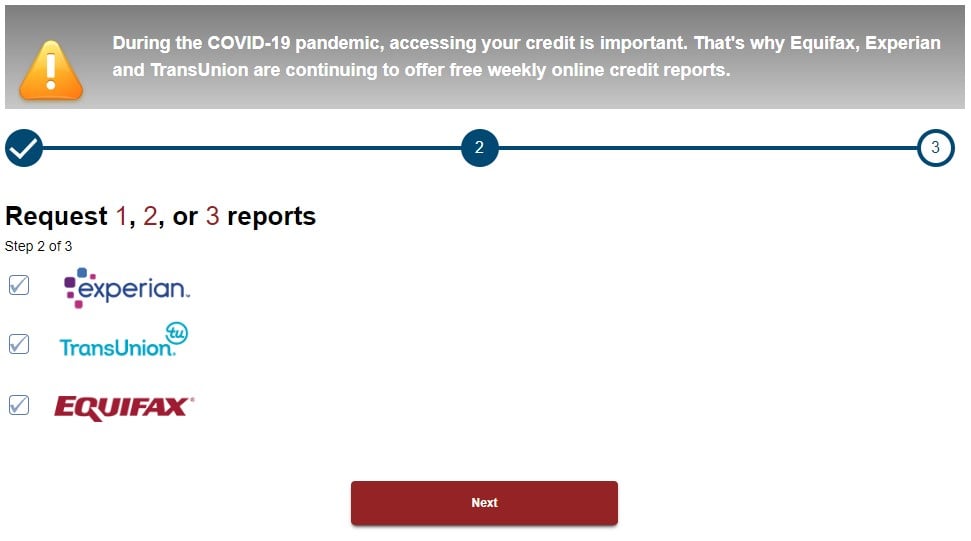

Tip 6: Get a Credit Report Three Times a Year

Each person can get one free credit report annually from each of the three major credit agencies from www.annualcreditreport.com.

Normally, I suggest staggering the report requests throughout the year, such as ordering one from Equifax in January, one from TransUnion in May, and one from Experian in September. Although your credit report won’t always match at each agency because some companies only request your credit report from one or two versus all three, this method at least gets you a peak into your credit reports more than once annually.

During the pandemic, this method isn’t necessary because the three credit bureaus are allowing individuals to request free weekly online credit reports.

Although freezing your credit should prevent unauthorized new credit from being opened, it only takes about 10 minutes to get a free credit report.

Plus, if you are a caregiver or helping an elderly person, you may spot issues or be alerted to old credit cards someone doesn’t use, but if they fall into the wrong hands, could be financially exploited.

It might help you clean up old credit accounts that aren’t being used; however, please be cautious about closing the oldest credit accounts because that could cause someone’s credit score to drop.

Asking for a free online credit report regularly is another way to learn about what credit is available to a senior and where exploitation may occur.

Tip 7: Block Solicitations

Solicitations are an easy entry point to financially exploit seniors.

If you are caring for an elderly person, I would consider doing the following:

- Stop commercial mail solicitations

- Stop unsolicited credit offers

- Eliminate robocalls

- Block calls from unknown numbers

- Do charitable giving together

Stop Commercial Mail Solicitations

If you want to decide what type of mail you get from marketers, you can register for DMAchoice.org.

Registering costs $2 and lasts for 10 years. Registering allows you to say whether you want credit offers, catalogs, magazine offers, donation requests, retail promotions, etc.

You can select which categories you want and whether you want to stop receiving mail from companies you’ve never purchased from.

There is even a do not contact list for caregivers, which allows caregivers to remove the name of individuals for whom they provide care.

Seniors are prone to responding to ads and marketing, which is why reducing or even eliminating the mail they receive can help combat the possibility of financial exploitation.

Stop Unsolicited Credit Offers

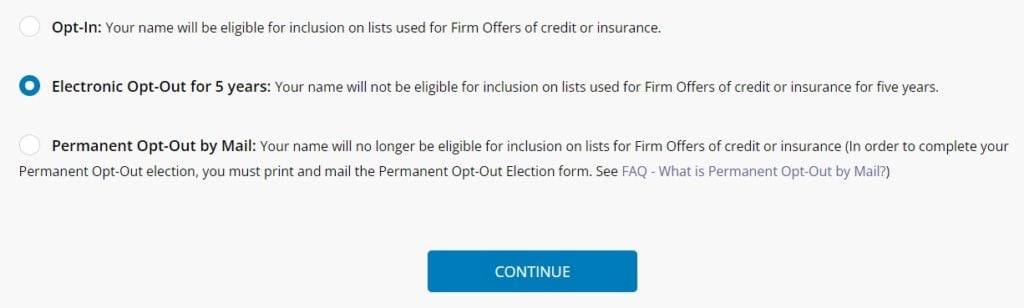

Did you know you can stop unsolicited credit offers?

While you can’t opt out for forever online, you can opt-out for five years using the online system. You can opt out permanently by mailing a form.

If your mailbox is anything like mine, you probably receive quite a few offers of credit or insurance offers each month.

If you are hoping to reduce the possibility of financial exploitation, stopping unsolicited credit offers may help. In my experience, more offers for products or services often confuse people with cognitive impairment. They often will respond to mail solicitations even if they already have insurance or don’t need credit.

Eliminate Robocalls

Eliminating robocalls isn’t easy, but there are a few steps you can take.

The first step is to register the senior’s home and mobile phones on the National Do Not Call Registry.

After that, you can adjust your phone settings. For example, Google has caller ID and spam protection on by default for Android phones, but you can also block spam calls within the settings. If you have an Apple phone, you can also silence calls or download an app that detects and blocks spam phone calls.

Verizon, AT&T, and T-Mobile also have their own anti-robocall tools. Most automatically work, but it’s worth talking to the carrier to see if there is anything else you need to do.

Silence Calls from Unknown Numbers

The last line of defense is to silence calls from unknown numbers.

Although the caller can still leave a message and will appear in the recent calls list, this might help prevent elder financial exploitation because many scammers are very convincing on the phone in real time and make actions sound urgent.

If your loved one gets a voicemail, perhaps you can have a system in place where you review the voicemails together to determine their legitimacy.

This is a tough tip to suggest because I know many seniors have doctors call from numbers that are not in your contacts list.

One idea is to ask what number may call to set up a doctor’s appointment and add that as a contact in advance. It requires more planning, but if it can reduce the likelihood of elder financial exploitation, the extra time and effort may be worthwhile.

Do Charitable Giving Together

One area I’ve seen things get out of hand is with charitable giving. Although it may not be senior financial exploitation in the traditional sense, I’ve seen elderly people forget what charities they are supporting and give more than intended.

One idea is to set up a charitable giving strategy with the senior in your life. You can pick a time each month to do the charitable giving and have them set aside any requests for charitable donations until that time. Alternatively, you could put the charitable giving on autopilot with recurring transactions.

It’s difficult because people have big hearts, but once you get on a charitable giving list, it’s really hard to get off the list. As those requests land in their mailbox, they may be tempted to write $50 here, $100 there, and before you know it, it’s more than they have ever given.

Something else you can consider is giving anonymously through a Donor-Advised Fund. It’s a great way to support the causes you want, but avoid being put on a charities solicitation list.

Tip 8: Stay in Regular Communication with Seniors

I know this seems obvious, but one of the best ways to catch elder financial exploitation early is to be in regular communication.

Unfortunately, it’s usually not enough to do a quick phone call or even a quick video chat.

The best way is to show up regularly on different days and at different times.

This way you can get a sense for who is around, how they spend their time, and how their living space looks.

You can ask about other caregivers, friends, advisors, or new romantic partners.

People should be suspicious and ask questions about anybody new in a senior’s life. You obviously want to be welcoming and thankful they have company, but you also want to be skeptical.

There is a fine balance between showing interest and gratitude for the socialization they get and trying to protect their best interests.

Since most financial exploitation is caused by someone close to seniors, it tends to be friends, love interests, and financial advisors who can do the most harm. They tend to be trusted people that are in positions of power.

Don’t forget to keep a close eye on the trusted people in their life.

Another area to watch is new services. I’ve seen seniors subscribe to very expensive investment newsletters, companionship websites, and random annual subscriptions.

Lastly, no family is going to agree 100% on what is best for the loved ones in your life, but I would encourage you to have regular, ongoing family conversations. By starting early, you can get a better picture of how someone is aging and handling their finances.

Sometimes a senior will share certain information with one child, but not another. By having conversations, you may get a more complete idea of how a loved one is doing.

Final Thoughts – My Question for You

Preventing elder financial exploitation feels like a game of whack-a-mole.

For every strategy, tip, or service that is created to combat it, scammers get better at scamming.

These tips are meant to help you think about what would be most useful in your situation. Some people may need all of them while others only need to take one step, such as setting up a trusted contact.

Depending on cognitive ability, age, and many other factors, you can assess your situation and decide what is reasonable for your family and your current experiences. As life progresses, you can come back to these tips to possibly implement more of them.

Lastly, be kind if a loved one is scammed. They are likely embarrassed enough. Although you have every right to be angry and upset, try your best to do it in a setting away from your loved one. You want them to feel comfortable reaching out if something ever happens.

I’ll leave you with one question to act on.

Which tip will you implement to help prevent elder financial exploitation?

About the Author

Elliott Appel, CFP®, CLU®, RLP®, is a Financial Planner and Founder of Kindness Financial Planning, LLC, a fee-only financial planning firm located in Madison, WI that works virtually with people across the country. Kindness Financial Planning is focused on helping widows, caregivers, and people affected by major health events organize and simplify their financial lives, do proactive tax planning, and make sure insurance and estate planning is coordinated with smart investment advice.

Did you know XYPN advisors provide virtual services? They can work with clients in any state! Find an Advisor.

Share this

Subscribe by email

I'm a Financial Advisor — Here Is How I Organize My Bank Accounts

I'm a Financial Advisor — Here Is How I Organize My Bank Accounts

April 28, 2020

9

min read

A Millennial's Guide to Credit Reports

A Millennial's Guide to Credit Reports

July 28, 2018

4

min read

How To Easily Monitor Your Credit

How To Easily Monitor Your Credit

April 02, 2019

4

min read