These Related Stories

Share this

.png?width=554&name=BLOG%20IMAGES%20TEMPLATE%20(28).png)

6.5 MIN READ

Every person who is about to attend college should know about the Free Application for Federal Student Aid and the process to apply. October means that the FAFSA applications are open for 2022-2023. Our video blog is going to cover commonly asked questions and 4 FAFSA tips.

What is FAFSA and how does it work?

The Free Application for Federal Student Aid (FAFSA) is the official form that all incoming and returning college students fill out for the next academic year. The FAFSA is a prerequisite for federal student loans, grants, and work-study, and may be required by colleges before they distribute their institutional aid to students.

In order to determine the financial need of a family, the FAFSA asks a number of questions about a family’s income, the student’s income, assets, and other factors such as how many children are in the family. It then comes up with an Expected Family Contribution (EFC). In July 2023, EFC will be renamed the Student Aid Index (SAI) to clarify its meaning. Based on the information you supply on the FAFSA will determine if you qualify for need-based aid, non-need-based aid, or some combination of the two.

Is it free money?

The FAFSA is an application used to determine your eligibility for receiving a federal loan. There are three types of financial aid that students may be eligible for. Some of this financial aid is free money, some must be earned through work, and some must be repaid.

How much will FAFSA give me?

The amount of money that you receive is dependent on what they determine to be your financial need. The average amount is around $5,000.

Who qualifies for FAFSA?

To qualify for various forms of federal student aid, you generally need to have some sort of financial need, be a U.S. citizen or eligible noncitizen, and be enrolled in an eligible degree or certificate program at a college or career school. However, there are more eligibility requirements based on the type of financial aid.

Tip #1: How do I get started with the FAFSA Application?

First, you and your student will each need to obtain a Federal Student ID, FSA ID, (which you can do online by following the instructions at studentaid.gov. Once you have an FSA ID, you can use the same one each year.

Secondly, you will need to submit the FAFSA. The fastest and easiest way to submit it is online at studentaid.gov. The online FAFSA allows your tax data to be directly imported from the IRS, which speeds up the overall process and reduces errors. The site contains resources and tools to help you complete the form, including a list of the documents and information you’ll need to file it. Students must submit the FAFSA every year to be eligible for financial aid (along with any other college-specific financial aid form that may be required, such as the CSS Profile). Any colleges you list on the FAFSA will also get a copy of the report. There is no cost to submit the application. It will take about 45-60 minutes to complete and it’s best if you complete it with your student.

Tip #2: How does the FAFSA calculate financial need?

The FAFSA looks at a family’s income, assets, and household information (for example, family size) to calculate what a family can afford to pay. This figure is known as the EFC, or expected family contribution. All financial aid packages are built around this number.

When counting income, it uses information in your tax return from two years earlier. This year is often referred to as the “base year” or the “prior-prior year.” For example, the 2022-2023 FAFSA will use income information in your 2020 tax return, so 2020 would be the base year or prior-prior year.

When counting assets, it uses the current value of your and your child’s assets. Some assets are not counted and do not need to be listed on the FAFSA. These include home equity in a primary residence, retirement accounts (e.g., 401k, IRA), annuities, and cash-value life insurance. Student assets are weighted more heavily than parent assets; students must contribute 20% of their assets vs. 5.6% for parents.

Your EFC remains constant, no matter which college your student attends. The difference between your EFC and a college’s cost of attendance equals your student’s financial need. Your student’s financial needs will be different at every school because of the cost of attendance.

After your EFC is calculated, the financial aid administrator at your student’s school will attempt to craft an aid package to meet your child’s financial need by offering a combination of loans, grants, scholarships, and work-study. Keep in mind that colleges are not obligated to meet 100% of your child’s financial needs. If they don’t, you are responsible for paying the difference.

– What documents will I need to file?

U.S citizens will need their Social Security number, driver’s license number, and tax and income records. The FAFSA checklist can be useful to look at in advance to make sure that you have all of the documents together before you fill out the application.

Tip #3: Should I file the FAFSA even if my student is unlikely to qualify for aid?

Yes, you should probably file a FAFSA even if your student is unlikely to qualify for aid. There are two good reasons to do this.

- All students attending college at least half-time are eligible for unsubsidized federal student loans, regardless of financial need or income level. (“Unsubsidized” means the borrower, rather than the federal government, pays the interest that accrues during school and during the grace period and any deferment periods after graduation.) If you want your child to be eligible for this federal loan, you’ll need to submit the FAFSA. But don’t worry, your child won’t be locked into taking out the loan. If you submit the FAFSA and then decide your child doesn’t need the student loan, your child can decline it through the college’s financial aid portal before the start of the school year.

- Colleges typically require the FAFSA when distributing their own need-based aid, and in some cases as a prerequisite for merit aid. So filing the FAFSA can give your child the broadest opportunity to be eligible for college-based aid. Similarly, many private scholarship sources may want to see the results of the FAFSA.

Tip #4: FAFSA Application Timeframe and Deadlines 2022-2023

When can you apply for FAFSA 2022?

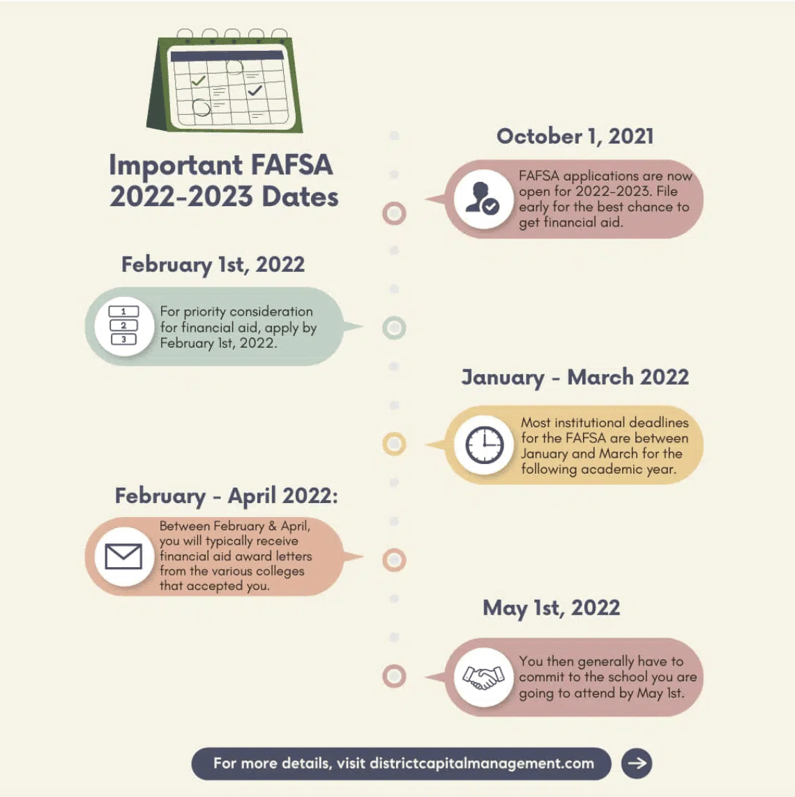

You need to complete the FAFSA form between October 1, 2021, and June 30, 2022, to be considered for federal financial aid for 2022-2023,

While you don’t need to complete the FAFSA by October 1, it is a good idea to file it as early as possible in the fall because some federal aid programs operate on a first-come, first-served basis. Colleges typically have a priority filing date for both incoming and returning students; the priority filing date can be found in the financial aid section of a college’s website. You should submit the application before that date.

What are the three FAFSA deadlines you must know?

There are federal, state and school deadlines. The FAFSA deadline set by the federal government is June 30, 2023 for the 2022-2023 school year. Any corrections or updates to your FAFSA application must be made by September 10, 2023. Colleges and states can set their own earlier FAFSA deadlines. It’s important to look at all of the deadlines to make sure that you apply on time. The earlier you apply, the better chance you have of receiving financial aid.

Other important FAFSA dates to be aware of:

- February 1st: for priority consideration for financial aid, apply by February 1st, 2022.

- January – March: Most institutional deadlines for the FAFSA are between January and March for the following academic year. Some schools have deadlines as early as the second week in January so it is best to get your application in early.

- February – April: Between February and April, you will typically receive financial aid award letters from the various colleges that accepted you.

- May 1st: You then generally have to commit to the school you are going to attend by May 1st.

Also, if you have not applied for financial aid for the 2021-2022 academic year then you have until June 30, 2023 to apply.

Is FAFSA first come first serve?

File early for the best chance to get financial aid. Many states disperse money until they run out so the earlier you apply, the higher chance you have of receiving financial aid.

My parents are divorced. Which parent should fill out the FAFSA application?

The parent who you have lived with for the last 12 months should be the one who fills out the FAFSA application. If your parents still live together, then you will need information from both parents.

Can I make changes to my FAFSA once it has been submitted?

Yes, you can make changes to your FAFSA if you find any errors and need to update information. Simply sign in to fafsa.ed.gov and then go to the “My FAFSA” page and then click on “Make FAFSA Corrections”.

When will I receive my FAFSA results?

You should receive your Student Aid Report around 3 days to 3 weeks after you submit the FASFA form.

Start your application for FAFSA 2022-2023 today!

Fill out the FAFSA early, even if you think you don’t qualify, so you’ll know your EFC and evaluate the different financial aid packages and the implications at each school. Sometimes the more expensive school may be a better deal. Most families are eligible for some form of federal financial aid for college.

If you are interested in ways to save and pay for college, come back soon as we are creating an entire series on saving for college. Lastly, if you are saving for college, you should have a strategy in place to maximize your money and resources.

About the Author

About the Author

Alvin Carlos, CFP®, CFA is an investment advisor and fee-only financial planner, in Washington, D.C that works with clients across the country. He has a Master’s degree in International Relations from SAIS-Johns Hopkins. Alvin is a partner of District Capital, a financial planning firm designed to help professionals in their 30s and 40s achieve their financial goals through smart investing, reducing taxes, retirement planning, and maximizing their money.

Did you know XYPN advisors provide virtual services? They can work with clients in any state! View Alvin's Find an Advisor profile.

Share this

Subscribe by email

7 Ways Childfree Financial Planning is Different

.png)

7 Ways Childfree Financial Planning is Different

January 11, 2022

6

min read

Good Financial Reads: When to and How To Reduce Capital Gains Taxes

Good Financial Reads: When to and How To Reduce Capital Gains Taxes

March 24, 2023

2

min read

Kids Savings Accounts

.png)

Kids Savings Accounts

December 31, 2019

6

min read