These Related Stories

Share this

8.5 MIN READ

Investors just went through one of the toughest investment years in history. This was a marked change from the 2019-2021 period which saw strong stock and bond returns despite the pandemic. The question on everyone’s mind is: “2022 was tough, will 2023 be better for investors?”. I don’t like “year-ahead outlook” reports. I’ve read hundreds of them over the years and they’re often obsolete by the end of January. Instead of trying to predict what 2023 might look like, I thought I’d share what’s on our mind and how that might affect investors in the New Year.

How Bad Were Investment Returns in 2022 Compared to History?

Stock investors have endured several years worse than what we saw in 2022. The S&P 500 index just averted bear market territory by finishing 2022 -18.5%. There have been a half-dozen years worse than 2022 for the S&P 500.

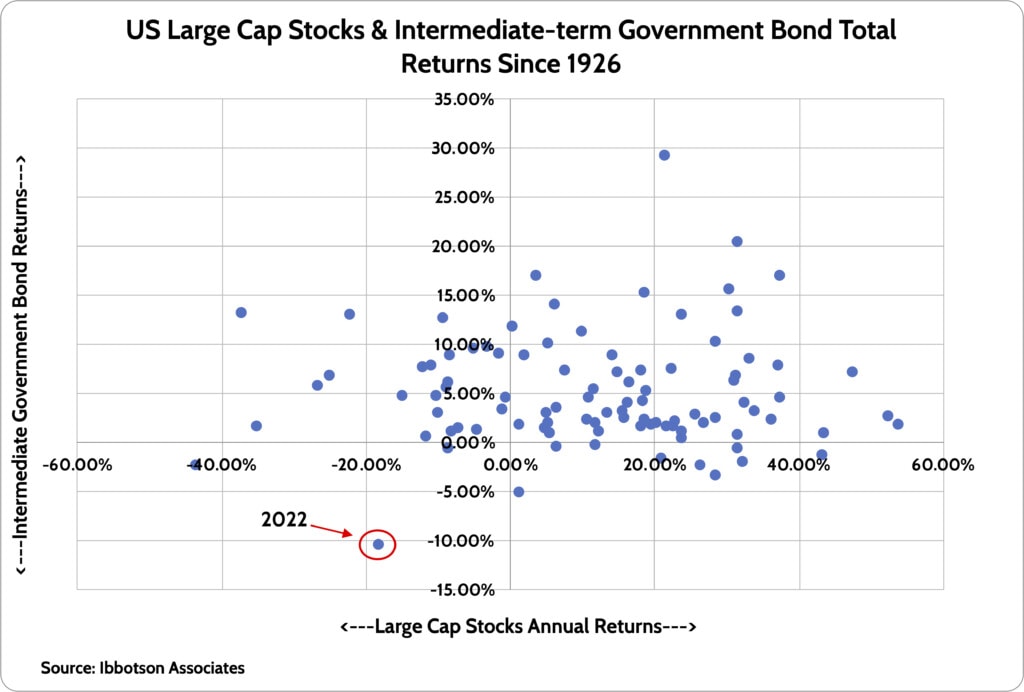

What was truly unique about 2022 for investors is the performance of bonds. We have total return data for intermediate-term U.S. Government bonds going back to 1926. By “intermediate-term,” I mean bonds that mature in 5-7 years. For these bonds, 2022 was the worst year ever.

When we combine annual stock and bond returns on a scatter plot, you can see that 2022 was truly an outlier.

Why did bonds have such a terrible year? It’s all because of the ‘unconventional’ monetary policy the Federal Reserve and other global central banks have engaged in since the Great Financial Crisis of 2008. By aggressively buying bonds as part of their Quantitative Easing policy, they pushed interest rates to some of their lowest levels ever. Another way to put this is that the Fed artificially boosted bond prices, which benefitted investors and borrowers for many years.

One of my favorite charts to show the insanity of monetary policy from 2008 to 2021 is to look at the total value of global debt with NEGATIVE yields. After peaking at nearly $18 trillion, the total value of negatively yielding debt is rapidly approaching zero.

Unwinding this insanity is the key reason bonds suffered so much in 2022. Going from extremely low yields to more normal yields meant lower bond prices. I’ll talk about the outlook for rates a bit later.

What follows is a somewhat random set of thoughts that we think are important to investors heading into 2023.

Will There Be a Recession in 2023?

There was a lot of talk about the economy being in recession in the middle of 2022. While official government statistics showed two quarters of economic contraction, there really wasn’t a recession. Employment levels are still very strong and consumer spending remains strong.

In recent blog posts I’ve talked about the potential for a recession in 2023. It may happen or it may not, or maybe it doesn’t happen until 2024. But it’s worth explaining why I have that belief.

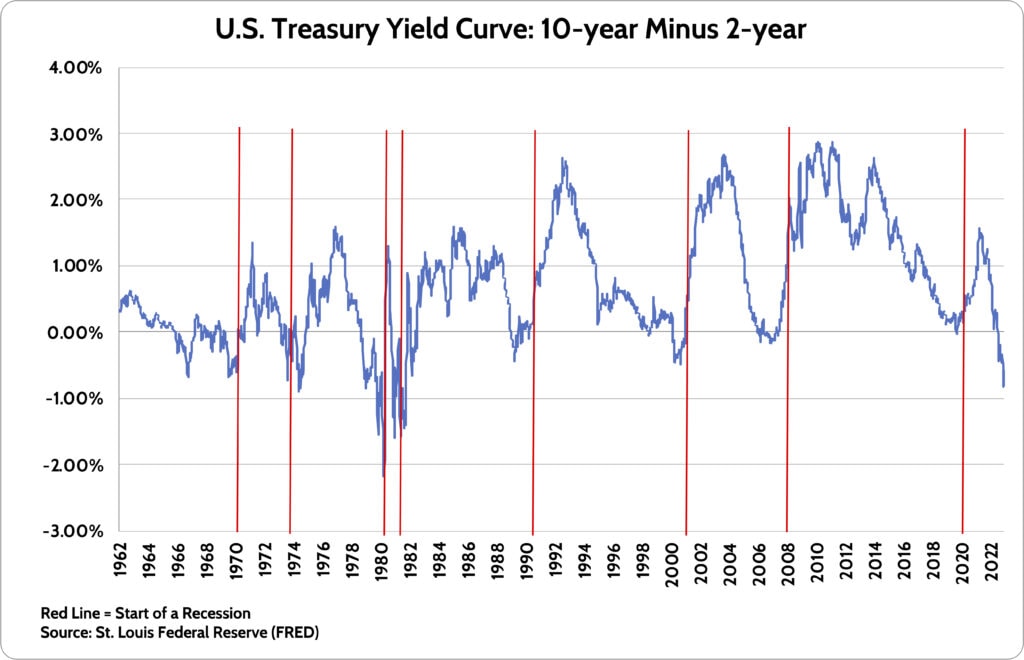

The most important reason is that the government bond yield curve is inverted. In plain English, bond investors believe the Federal Reserve when it says it will hike short-term interest rates towards 5.00% in 2023. But these same investors expect lower interest rates beyond two years. This suggests a belief that the Fed will have to cut rates at some point, which they only do in recessions.

The above chart looks at the most common way investors look at the yield curve. 10-year government bonds are the market’s expectation of “normal” interest rates. 2-year government bond yields are what the market actually thinks monetary policy from the Fed will look like in the short-term.

The red lines in the chart show the start of a recession. If you look closely, you’ll see that every time you see the blue line go below 0% (except 1966) you see a red line happen soon after. Today’s yield curve is as inverted as it has been since the early 1980s. That is the last time we had a real inflation battle on our hands.

Investors have to ask themselves, “Will this time be different?”. Will we avoid recession after an inverted yield curve signal for the first time in 52 years? My hunch is we won’t.

This hunch is driven by the fact we’ve had one of the most aggressive interest rate hike cycles on record. The U.S. economy had operated with near 0% rates for over a dozen years. Suddenly, we’ve gone from 0% to near 5% in 12 months.

I don’t think rates can go up this much this quickly without consequence. Interest rates drive everything in the economy. Home prices and building activity are going to take a hit. Large companies that feasted on cheap debt to buy back their stock will have to pay that debt off or roll it over at much higher rates. The consequences are many.

Will the Fed “Pivot” and Stop Hiking Rates??

The debate du jour in the market today is when the Fed will stop hiking interest rates. Most participants think they will hike 2-3 more times in early 2023 and then stop. I would agree with that assessment.

What comes after that pause in rate hikes is the real question. The vast majority of today’s investors only know about one thing: the economy goes into recession, the Fed cuts rates aggressively, and stocks go up. That’s been the playbook for over two decades.

My thesis is that it’s not that simple this time because of the inflation problem we have. Sure, the inflation rate will come down in 2023 as supply chains normalize and we lap some of the huge inflation we saw in 2022. But I don’t think we’re going back to a world of 1-2% inflation soon.

The biggest challenge the Fed has economically and politically is the jobs market. They know full well that strong wage growth leads to higher future inflation. And that’s exactly what we’re seeing with extremely strong wage growth, particularly for those in the bottom half of wage earners.

Summarizing:

1) Inflation is an enormous problem for the economy…

2) Interest rate hikes have done nothing to loosen up labor markets. As evidenced by a very low unemployment rate and strong wage growth…

3) The longer the labor market remains tight, the higher the odds are of a “wage-price spiral” in coming years, which would keep inflation high…

This puts the Fed in a difficult position. If they pause rate hikes and the economy continues to hum along with low unemployment, then future inflation is likely to be higher because of strong wage gains for workers. Then what? Let’s speak the truth out loud: The Fed wants people to lose jobs so the labor market loosens up, wage growth slows, and inflation falls back to their made-up “target” of 2% inflation. That’s the unvarnished truth, something you’ll never hear out of their mouths because of the political firestorm that would ensue.

The risk I see for the market in 2023 is that the Fed will be forced to hike rates higher than 5.0% and keep them there for longer than investors expect. Bond investors are baking in interest rate cuts of 1.00% by the middle of 2024. I’m not one to fight the market. But that seems hopelessly optimistic absent a severe recession and spike in the unemployment rate.

A potential recession and the path of Federal Reserve policy are the two headwinds that stock investors face in 2023. If the economy is strong and a recession doesn’t happen, then the Fed will keep rates high, which is a headwind for stocks. But if a recession happens, then stocks would struggle with the drop in company profits. Much like 2022, we continue to see the balance of risks outweighing potential rewards for stocks.

High Quality Bonds Should Perform Better in 2023

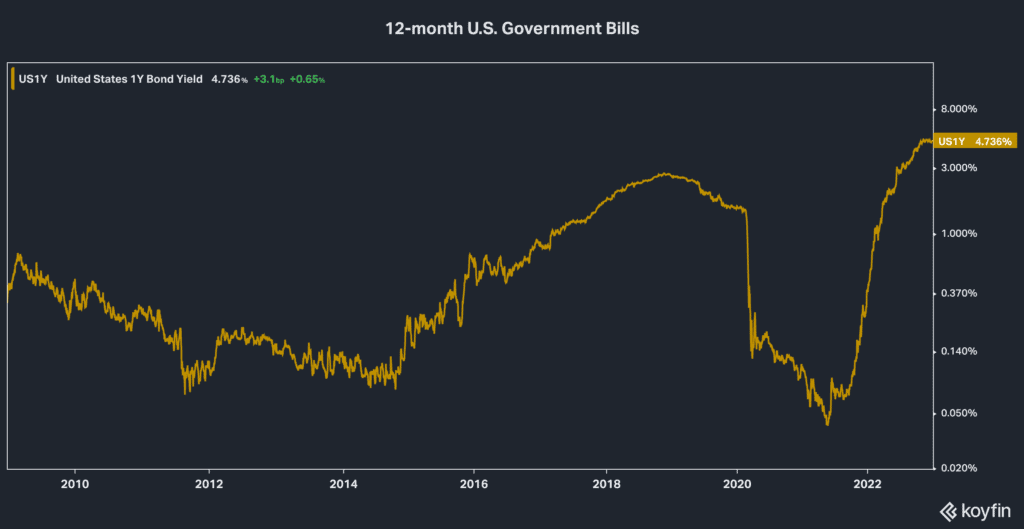

The outlook for Bonds looks better heading into 2023. Honestly, it can’t really get worse than it was in 2022. My reasoning for expecting better performance from Bonds is that short- and long-term interest rates are at much more reasonable (and higher) levels than they were a year ago.

Higher interest rates equals less bond price risk, unlike last year. On January 1, 2023, an investor can earn 4.75% on a one-year, risk-free government bond. Boring savings accounts at some online banks will now pay you close to 3.30%. In short, investors are getting paid to do nothing with their money for the first time in nearly 15 years.

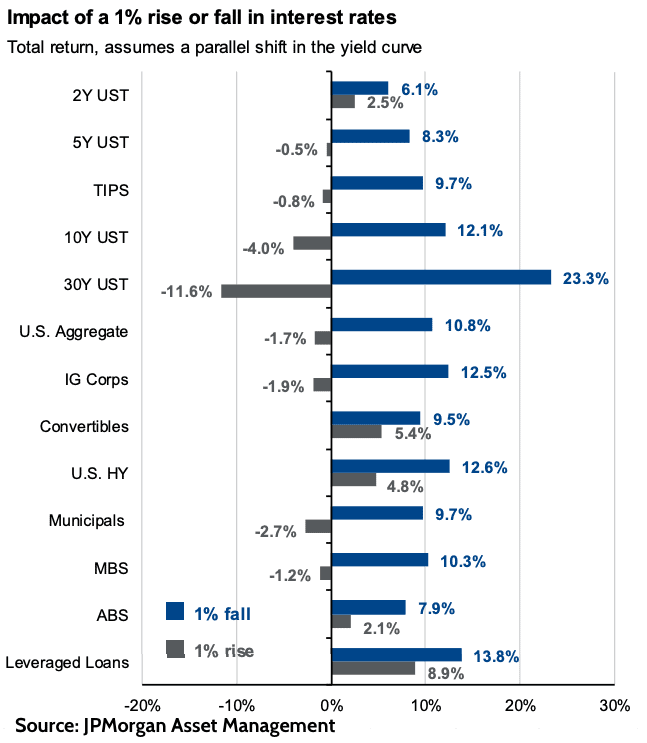

JP Morgan Asset Management publishes a handy chart showing the potential impact on bond returns from a 1% rise/fall in interest rates. As you can see, the price risk from a 1.00% rise in interest rates is small. That is unless you’re invested in very long-term bonds such as 30-year U.S. Treasury bonds.

Looking at the chart, it looks like bonds of all types are great values. But I don’t think that’s the case. For ultra-safe U.S. Treasury bonds (above: “USTs”) I’m positive on the return outlook for 2023. But when we’re talking about corporate bonds, leveraged loans, and high yield “junk” bonds, the outlook remains uncertain.

Non-government bonds are influenced by the level of interest rates AND the perceived credit risk of those bonds compared to risk-free government bonds. The “spread” between the yield you earn on a non-government bond compared to a government bond can significantly affect investor returns.

With a potential recession on the horizon, caution is warranted with non-government bonds. If a recession happens, then the “spread” I just spoke about will rise. This will negatively affects the prices of non-government bonds.

The good news for FDS clients is that we’ve taken steps over the last 18 months to reduce interest rate risk AND credit risk in client bond portfolios. While we’re seeing increasing value in longer-term government bonds that are sensitive to interest rates, it feels early to “chase yield” in non-government bonds, as tempting as the interest rates might be.

Will 2023 Be Better for Investors?

Given the caution above, it’s no surprise that we continue to take a cautious approach with client investments. The most notable move took place at the tail-end of the summer rally in stocks. Then, we moved 10% of client funds out of stocks and into money market funds which now yield 4%.

Using cash as a strategic investment allocation tool will continue into 2023. The ‘cost’ of sitting in cash is a lot lower than what it was when everyone was earning 0% on their savings.

As noted above, there’s increasing value in parts of the bond market. Depending on where longer-term interest rates go, we may seek to add interest rate risk (“duration”) back to bonds. These were first reduced two years ago. It will probably take some time to see better value in the non-government bond space. But we’re always ready to take advantage of opportunities when we see them.

Finally, on the stocks side of the ledger, we think being nimble in adding & reducing stocks exposure will be the name of the game. Markets have proven quite volatile and given the economic uncertainties out there, we wouldn’t be surprised to see that continue.

Stocks are not a screaming value, to be frank. A lot of the large cap technology fluff that surged in 2020 and 2021 came down dramatically in 2022. However, that doesn’t mean those stocks are cheap.

A lot will depend on whether we have a recession and how deep the profit recession will be for Corporate America. Stocks rarely find a bottom until investors are comfortable they can see a bottom on corporate profitability.

One of the hardest things about investing is being patient. As I scan the blogs I’ve written over the last 2+ years, they always seem to have a negative bent to them. That’s not because I’m a negative person! We are in one of the most important shifts in the investment environment in our lifetimes. That takes time to play out.

Value will emerge across the investment landscape at some point. And we’ll be happy to “go long” when that happens. But at FDS, protecting our clients is job #1. Your dreams, your goals, your financial life are not to be trifled with. We can’t guarantee anything for clients. But we can give it our all every day to help move the odds in clients’ favor.

.png?width=324&height=324&name=Blog%20Contributor%20Headshot%20Style%20(400%20%C3%97%20400%20px).png)

About the Author

Rob has over 20 years experience in the financial services industry. Prior to joining Financial Design Studio, he spent nearly 20 years as an investment analyst serving large institutional clients, such as pension funds and endowments. He had also started his own financial planning firm which was eventually merged into FDS.

Did you know XYPN advisors provide virtual services? They can work with clients in any state! Find an Advisor.

Share this

Subscribe by email

Recapping 2020 Investment Returns and Looking Forward to 2021

Recapping 2020 Investment Returns and Looking Forward to 2021

December 22, 2020

6

min read

Tips for Investing in an Election Year

Tips for Investing in an Election Year

October 20, 2020

7

min read

Managing Interest Rate Risk In Your Bond Investments

Managing Interest Rate Risk In Your Bond Investments

September 13, 2022

10

min read